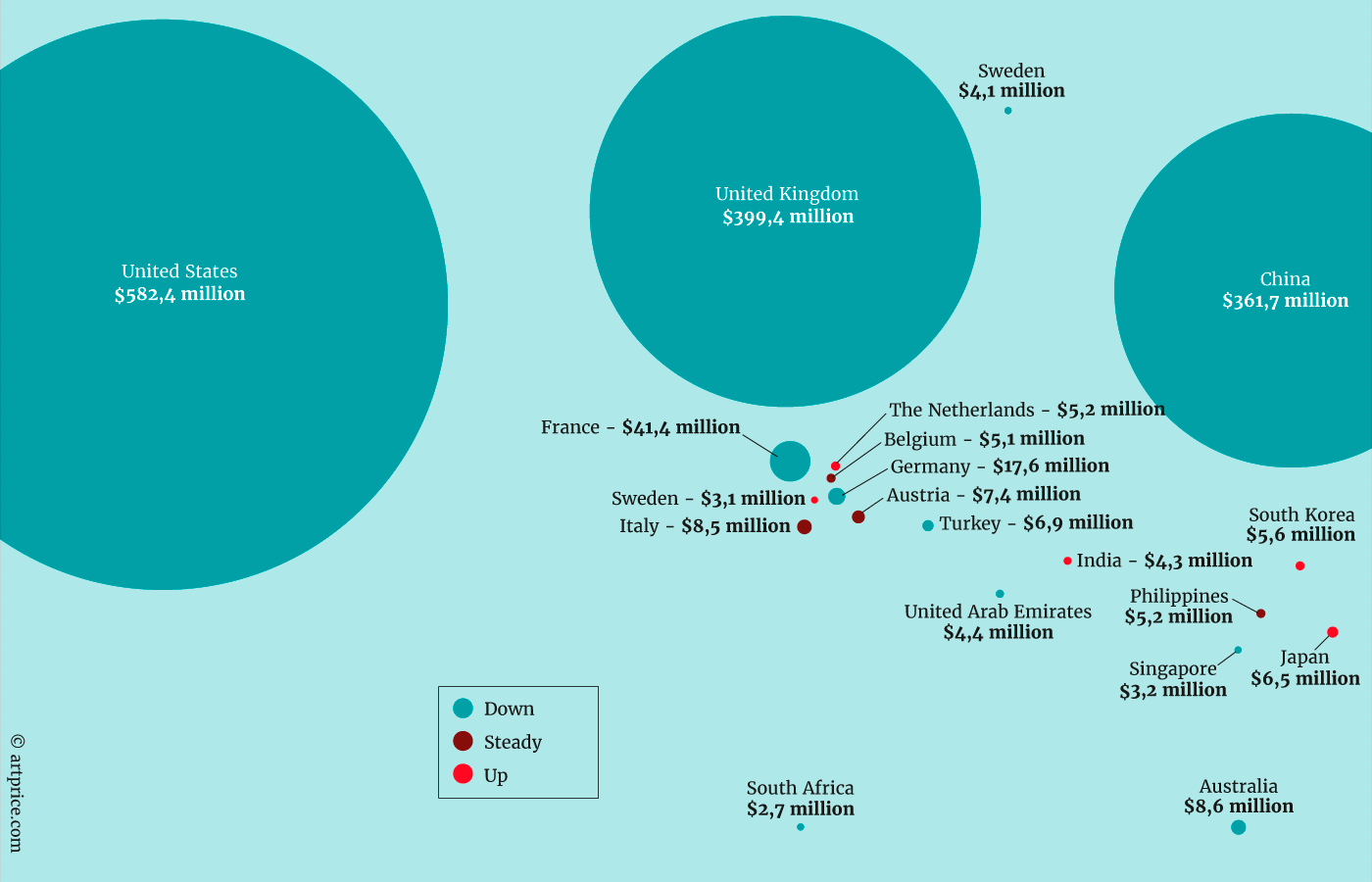

Market geography

With the Chinese art market undergoing a profound reorganisation, the USA and the UK saw their combined market share of the global Contemporary art market expand by 5 percentage points. Together they now account for 65% of global Contemporary art auction turnover. This strength reflects their capacity to propose a dense offer (a quarter of all Contemporary works go through London and New York), a quasi-monopoly of the ultra-high end of the market and their capacity to attract the world’s most powerful buyers.

The USA is the strongest marketplace in the world for Contemporary art generating $582 million over our 12-month period and accounting for 38% of the global market. Almost 95% of this total is generated in New York, although Florida and Texas occasionally produce good auction results as well. In the July 2015 – June 2016 period, the USA’s turnover on this segment contracted by 24%, but it still retains its considerable lead over the rest of the world.

The United Kingdom accounted for a quarter of global Contemporary art auction turnover and despite a 10% contraction to $399 million, it was $40 million ahead of China. The People’s Republic lost the 2nd place it just managed to win last year; but that is only part of the Chinese picture since the country has just returned as the undisputed leader of the global art market as a whole, as discussed in Artprice’s H1 2016 Report.

Geographic Distribution of Contemporary Art Sales

July 2015 – June 2016

China’s restructuring market

The stats for China’s art market over the past year indicate a profound reorganisation of art buying in the country. After the general correction that began in early 2014 collectors refocused their attention on “historic” artworks, a movement that primarily impacted sales of Contemporary art. The result was a -47% contraction of China’s Contemporary art market and the volume of transactions was halved. Nevertheless, the unsold rate has remained stable.

Chinese collectors do not appear to have deserted auction rooms, but they have definitely refocused on the big names in art history. A number of recent transactions have reminded us of their presence on the Western art market as well as their purchasing firepower: Chinese buyers acquired three European masterpieces this year: Claude Monet’s Bassin aux nymphéas, les rosiers for $20.4 million, Vincent Van Gogh’s L’allée des Alyscamps for $66.3 million and Amedeo Modigliani’s Nu Couché for $170 million.

Although China is today the world’s strongest art marketplace (all periods combined), it came third in the Contemporary art segment where it accounted for just 24% of global auction turnover compared with nearly 33% the previous year.

However, this contraction has made only a relatively small impact on the evolution of China’s Contemporary art market which is still showing a +470% increase for the past six years alone. China’s reorganisation will doubtless continue after the Draconian measures and regulations introduced by the Chinese government, including extremely strict legislation introduced two years ago to eradicate unpaid (false) bidding.

China’s cities ranked by Contemporary art auction turnover

| City | Auction Revenue | Sold Lots | Best result | |

|---|---|---|---|---|

| 1 | New York | $551,288,264 | 3 075 | $57,285,000 |

| 2 | London | $396,516,986 | 3 561 | $16,346,086 |

| 3 | Hong Kong | $147,119,080 | 1 347 | $5,443,800 |

| 4 | Beijing | $132,336,961 | 2 902 | $5,954,355 |

| 5 | Paris | $37,020,653 | 4 293 | $3,028,112 |

| 6 | Guangzhou | $26,463,136 | 907 | $1,367,925 |

| 7 | Shanghai | $15,872,066 | 495 | $1,044,888 |

| 8 | Hangzhou | $12,633,575 | 216 | $1,209,754 |

| 9 | Taipei | $11,382,617 | 358 | $852,564 |

| 10 | Vienna | $7,361,495 | 681 | $491,006 |

July 2015 – June 2016 / © artprice.com

Other Asian markets

Indonesia, the Philippines and South Korea all possess very dynamic Contemporary art scenes, but they are struggling to emancipate themselves from the local domination of Hong Kong and Singapore. Each of these three markets essentially consists of national artists. Unfortunately as soon as these local artists achieve some level of international recognition, their best works end up being sold through Hong Kong and Singapore.

This year again, the Indonesian market (which totalled $312,000 in turnover) has not benefited from the excellent results of I Nyoman Masriadi (b. 1973) and Christine Ay Tjoe (b. 1973), two artists who both rank in our global Top 500.

The Philippines on the other hand has managed to rake back part of the market created by their best artists. For example, the turnover generated by Ronald Ventura (b. 1973), the countries most eminent 3-D creator, is now 70% Hong Kong and 30% Manila. Until 2010, Hong Kong and Singapore captured 100% of the artist’s auction turnover. Another example is the 40% of turnover generated by the new Filipino star Jigger Cruz (b. 1984) that has also remained in Manila.

By repatriating the sales of these artists (whose prices had started to rocket abroad), the Philippines have given birth to a vigorous domestic market capable of attracting the most powerful collectors. In so doing, the country has risen to 12th position in the global ranking of national marketplaces and is today ahead of certain historical marketplaces like the Netherlands (13th) and Belgium (14th).

South Korea has followed a similar and even more impressive path. Its $5.5 million of Contemporary art auction turnover last year represented a spectacular 51% increase over the previous 12-month period. This growth was generated not only by the sale of works by their domestic artists (of whom 7 are in our Top 500 ranking), but also by a number of excellent results for Western artists.

Top 10 Contemporary art results in South Korea

| Artist | Work | Price | Date | Sale | |

|---|---|---|---|---|---|

| 1 | Damien HIRST (1965) | Love, Love, Love, Love (1998) | $244,970 | 15 Dec 2015 | K-Auction SEOUL |

| 2 | Sangki SON (1949-1988) | Nothing but Roses (1986) | $194,480 | 15 Dec 2015 | K-Auction SEOUL |

| 3 | Chi Gyun OH (1956) | Persimmons (2010) | $139,400 | 16 Sep 2015 | K-Auction SEOUL |

| 4 | Sangki SON (1949-1988) | The City of Labour-Traffic Lights (1980) | $125,630 | 28 Jun 2016 | K-Auction SEOUL |

| 5 | Sangki SON (1949-1988) | “Early Spring-Extra” (1987) | $124,740 | 16 Mar 2016 | Seoul Auction SEOUL |

| 6 | Dong-Youb LEE (1946-2013) | Situation B (1974) | $104,923 | 25 Mar 2016 | K-Auction SEOUL |

| 7 | Anselm REYLE (1970) | Untitled (2007) | $93,500 | 15 Dec 2015 | K-Auction SEOUL |

| 8 | Sangki SON (1949-1988) | In Bugahyeon-dong – Sisters (1986) | $76,670 | 15 Dec 2015 | K-Auction SEOUL |

| 9 | Hernan BAS (1978) | Case Study (Anton, The Best Present) (2014) | $68,006 | 29 May 2016 | K-Auction SEOUL |

| 10 | Julian OPIE (1958) | Carlos, Schoolboy (2007) | $67,562 | 9 Mar 2016 | K-Auction SEOUL |

July 2015 – June 2016 / © artprice.com

Europe finds a balance

On the whole, the Contemporary Art market’s European capitals have resisted the slowdown with slight increases in Contemporary art turnover in Vienna ($7.3 million), Amsterdam ($4.9 million), Berlin ($4.2 million), Brussels ($3.2 million) and Milan ($1.6 million). The market’s “hesitation” has mainly impacted high-end prestige sales and this is not a sector where these cities have any real weight.

Germany’s total was however down 19% to $17.6 million. Nowadays a relatively small marketplace for Contemporary art, Germany’s contraction was nevertheless somewhat worrying. It posted the sharpest contraction on the European continent with an unsold rate up from 44% to 55%.

Italy’s unsold rate was also worryingly high. Despite maintaining its 7th position on the global map (with turnover of $8.5 million), nearly half of the Contemporary art lots offered in Italy over the year remained unsold.

Lastly, France held its fourth position in the global Contemporary art market with a turnover total of $41.4 million, down -6.8% versus the previous year. However, given the current context this contraction seems perfectly natural. Transaction volumes remained high in France and once again the country exchanged more works of Contemporary art than either the UK or China. Two results above the million-dollar threshold were hammered in Paris this year, proving that the French capital has managed to keep at least one foot in the high-end market.

The influence of national markets

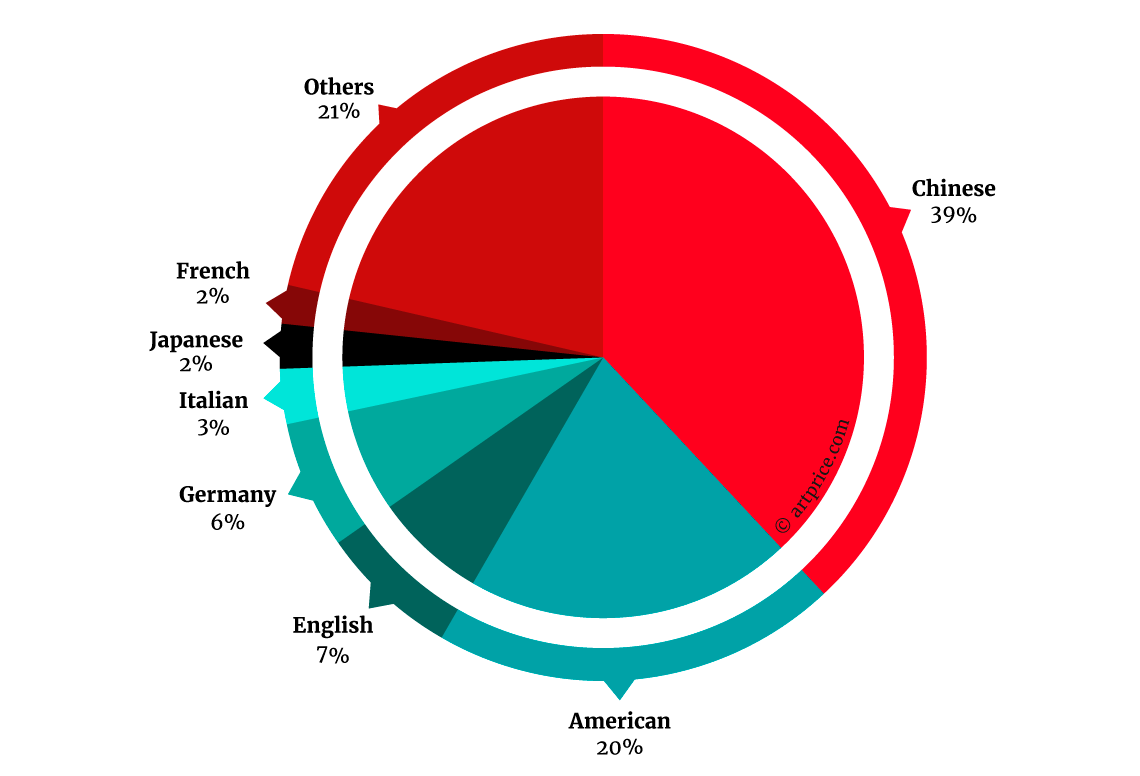

Our ranking of the global top 500 artists in terms of annual auction turnover reveals the influence of strong national markets on the results of artists from those countries: 99 Americans and 187 Chinese artists account for nearly 60% of the Top 500. And the domination of the United States is particularly visible at the top of the ranking with five artists in the Top 10, but just one Chinese artist.

However, compared with the strength of the London market, British artists are relatively unrepresented with only 36 names in the top 500, but several with very high rankings. The best-known of these are Peter Doig (ranked 5th), Damien Hirst (14th) and Antony Gormley (31st). Other British artists, less known to the general public, generated remarkable annual turnovers, like Lynette Yiadom-Boakye ($1.3 million), Harland Miller ($934,000), Hurvin Anderson ($796,000) and Adam McEwen ($600,000).

Germany has 31 artists in the Top 500 including 10 in the Top 100: Anselm Kiefer, Günther Förg, Martin Kippenberger, Neo Rauch, Sterling Ruby, Albert Oehlen, Thomas Schütte, Andreas Gursky, Rosemarie Trockel and Isa Genzken. Unfortunately the best works by the strongest German artists are generally sold in London and New York… an export trend that Berlin is now actively trying to prevent.

In total, these four nationalities account for 70% of the total turnover generated by the Top 500 artists. This leaves little room for artists of other origins. Italy, France and Japan each have around ten artists in the ranking and the numbers thin out for other nationalities: eight Belgians, seven Filippinos, five Russians, five Brazilians. Lastly, four Indians (Anish Kapoor, Subodh Gupta, Ravinder Reddy, Raqib Shaw) and three Spanish artists (Miquel Barcelo, Juan Munoz and Jaume Plensa) posted annual auction turnovers above $254,000 (the ranking’s minimum entry ticket).

Top 500 Artists Repartition by Nationality

July 2015 – June 2016

Although the concentration of the Contemporary art market in London and New York undoubtedly stimulates the prices of British and American artists, it also benefits foreign artists by inflating their prices to higher levels. In fact, more than half of both the US’s and the UK’s respective turnover totals is generated by foreign artists.

So while strong national markets benefit their respective national artists, that marketplace strength itself depends on the capacity to attract an international supply along with an international demand, which is of course is what the major auction houses are good at.

Majors auction houses post lower turnovers

Despite a 19% fall in sales turnover, Christie’s is still the world’s leading auctioneer for Contemporary art sales with a total for the year of $545 million. Its historical competitor, Sotheby’s, has been less affected on this segment, posting a small contraction of -2%. Despite a difficult year, the two international auction operators generated 61% of global Contemporary art auction turnover. Phillips, which has reiterated its third place with stable turnover versus the previous year ($160 million) is still a long way behind the two leaders.

In order to ensure price stability on the Contemporary art market, Christie’s and Sotheby’s restricted their ultra-high-end offer as soon as the first signs of market weakness became apparent. The very best works, usually sold with very substantial price guarantees, have been particularly rare over the period in question, and this essentially explains why Christie’s and Sotheby’s turnover figures contracted.

Top 10 auction operators in the world

| Market share | ||||

|---|---|---|---|---|

| Auction House | Auction Revenue | Sold Lots | Best result | |

| 1 | Christie’s | 36% | 5% | $57,285,000 |

| 2 | Sotheby’s | 25% | 4% | $13,914,000 |

| 3 | Phillips | 11% | 3% | $5,775,437 |

| 4 | Poly International | 4% | 2% | $2,627,635 |

| 5 | China Guardian | 3% | 1% | $5,954,355 |

| 6 | Beijing Council | 1% | 0% | $728,899 |

| 7 | Xiling Yinshe | 1% | 0% | $1,209,754 |

| 8 | Holly International | 1% | 0% | $1,367,925 |

| 9 | Bonhams | 1% | 1% | $758,924 |

| 10 | Artcurial | 1% | 1% | $398,790 |

July 2015 – June 2016 / © artprice.com

The global Top 10 ranking of auctioneers for the Contemporary art segment contains five Chinese operators. Their annual totals range from $12.2 million to $44.5 million. They are therefore still a long way behind the Christie’s-Sotheby’s-Phillips triumvirate.

In the West, Bonhams and Artcurial have remained in the top 10 auction houses with $11 million and $9 million respectively, each offering approximately 700 Contemporary artworks over the 12-month period.

The French market is still one of the world’s densest, most interesting and most diversified in terms of the type of works available. Ranked tenth in the world, Artcurial managed to double its Contemporary art turnover generating 23% of the French market on this segment. Cannes Enchères also doubled its turnover and Cornette de Saint-Cyr increased from $1.4 million to $2.3 million thanks notably to a drawing by Jean-Michel Basquiat — Cannon (Act 1) (1981) — that fetched $680,000. Lastly, Millon and Piasa remained neck and neck, each posting increases from $1 million to $1.9 million.

Although the French Contemporary art market is dominated by Christie’s and Sotheby’s (37% of the local market’s turnover), it shows that coexistence is possible between the international giants and the small- and medium-sized operators. Indeed, this year their complementarity has been beneficial to the overall stability of the market.

A strategic acquisition

In the Soft Power competition between China and the United States for art market supremacy, Taikang Life Insurance’s acquisition of 13.5% majority stake in Sotheby’s capital has raised eyebrows across the United States. Taikang’s CEO, Chen Dongshen, is also the outright owner of China’s no. 5 auction operator, China Guardian.

Tad Smith, Sotheby’s CEO stressed that the members of Sotheby’s board approved this strategic operation. Sotheby’s New York listed share price (the only listed auctioneer) posted a +52% progression from 1 January 2016 to mid-August, illustrating the confidence of financial markets in the art market.

China Guardian (whose Fine Art turnover reached $553 million last year) owns 24% of Taikang, which makes it China Guardian’s majority shareholder. The move has rekindled speculation about Poly Auction trying to acquire Bonhams in the UK.

Chen Dongshen’s acquisition of a majority stake in Sotheby’s is entirely consistent with his previous ventures. Twenty-five years ago he founded the China Guardian auction house, three years before starting Taikang Life Insurance. Taikang’s shareholders include Goldman Sachs (13%) and a Singapore-based investment company. Today aged fifty-nine, Chen Dongshen was born in Hubei province and holds a Doctorate in Economics from Wuhan University. He worked as Chief-Editor of a State-run economics journal before setting up China Guardian in 1993. He is married to Mao’s grand-daughter and has confessed that he meticulously studied Sotheby’s sales in Hong Kong to improve and enhance those conducted by China Guardian. Dividing his time between his passion for art and his insurance activities, he exhibits works of calligraphy and traditional Chinese paintings in his offices. In Beijing, the new headquarters of his auction company – the Guardian Art Center – will house a cultural complex with international visibility.

30.6

30.6